By Will Porter, Associate Director, Providence Independent Investment Advisory

First published on Livewiremarkets.com

In our December Quarterly Outlook Statement, I published the below article highlighting a higher required return from equities should we continue to extrapolate low bond yields and their impact on equity valuations. The key messages being, 1) if you are going to transfer the low yield to valuations it would be wise to also consider the volatility of that yield and allocate appropriately on a risk-adjusted basis; and 2) there are purer ways to gain access to duration if that is the return you are trying to capture.

Extract from Providence December 2019 Global Outlook and Strategy Document – “The Most Diversified in 20 Years”:

It is now consensus that the currently stretched equity market valuations (in fact valuations in general) are wholly justifiable due to low bond yields. As discussed in our previous post, this academically makes sense when using the dividend growth model of valuation. We also discussed how this will have significant implications for portfolio construction if you rely on this argument as the primary driver for increasing allocations to equities.

As an extension, we delve into the potential impacts that this assessment of valuation may have on expected equity market volatility should it become the markets primary source for deriving equity market valuations.

We will continue to use the example of a company, creatively named “XYZ Company”, that can grow its dividend at 4% p.a into perpetuity and will retain the equity risk premium of 5%. For relevance, we will use a 10-year bond rate of 1% in this analysis.

At these low levels of bond yield, the impact of changes in the bond yield on the implied valuation of our stock using the dividend growth model are even more significant. The table below demonstrates the impact of a 3.8bp (0.038%) move in the bond yield (the average daily bond yield change over the past 10 years) on our stock’s valuation at different levels of the 10-year bond yield. The output is what this means for the annualised volatility of this valuation metric and therefore the stock itself (ceteris paribus).

Our priority is to ensure that we are being adequately compensated for the risk that we are taking. At the current 10-yer bond yield of 1.00% the expected annual volatility could be assumed at 30.1% based on the dividend growth model, this compares to the experienced volatility of the S&P ASX 200 over the past 10 years of 14.2%. If we were to rely on this assessment of fair value and therefore the implications on expected Australian equity volatility, we would require more than double the historical return of the S&P ASX 200 over the past years to justify the additional risk.

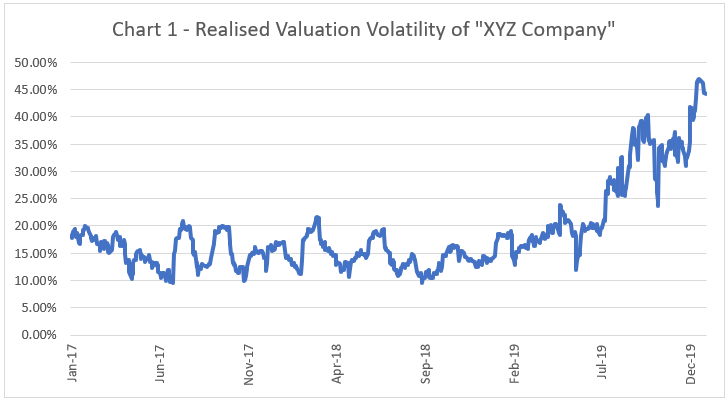

To put this into the real world, the below chart plots the valuation volatility of “XYZ Company” growing dividends at 4% with an Equity risk premium of 5%, using the actual daily 10-year bond yield experienced over the past 3 years and calculating the annualised 20-day volatility of that valuation (Chart 1).

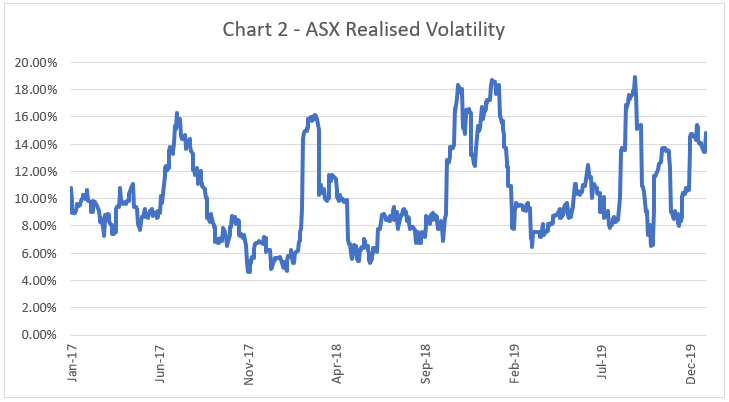

In theory, the annualised 20-day volatility of “Company XYZ’s” valuation has increased significantly as the bond yield has been volatile at a low level. In reality, we have seen very little movement in equity index volatility in Australia during this volatile period (chart 2) which is understandable given it is a far more diversified exposure than a single security, but this increase in volatility of growth stocks would be reflected at the index level somewhat. Therefore, we can reasonably conclude that this is not the sole metric that is relied on by the market.

In practice, it is unlikely that you would adjust your 10-year bond yield daily given the volatility that this introduces to your valuation (Chart 1). However, if the sole argument for equity exposure relies on a forecast of bond yields you should consider what underlying risk you are adding. It certainly sounds more like adding long duration, but if this is the risk you are trying to capture there are far purer ways to do so than via equities.

The purpose of this analysis is to suggest that the over-reliance on a single valuation metric can have significant impacts on other inputs that may be useful when constructing portfolios. We agree that lower bond yields can justify the elevated valuations that global equity markets are experiencing, however, we need to be aware that if this is the sole reason for elevated valuations we may need to increase our expectations for equity market volatility and measure this against our expected return.

We remain as diversified as we have ever been both across and within asset classes to try to mitigate the reliance on low bond yields to drive returns. We continue to focus on owning assets or employing managers that have a wide range of options to drive value.